The Hidden Cost of Credit Bureau Scores

- April 9, 2026

- Decisões de crédito

Why generic credit scores limit your growth in 2026, and how customized credit scores turn risk into a competitive advantage.

With Phase 4 of Open Finance now in effect, the consolidated PIX Parcelado system, and digital credit fintechs growing by 68% annually even in a high-interest-rate environment, the question is no longer whether your scoring model needs to evolve. It’s how much you’ve already lost by putting off this decision.

Introduction: The credit score that’s holding your business back might be the one you set yourself

There is a cost that doesn’t appear on the agency’s invoice. It doesn’t show up in the bad debt line of your income statement, nor in the credit desk’s monthly report. But it’s there, eroding margins, wasting customer acquisition costs, and handing market share on a silver platter to the competitor who made a different decision than you did.

This cost has a name: it’s the price paid by any company that uses an off-the-shelf credit score as if it were the ultimate analytical tool. Spoiler: it isn’t.

The major credit bureaus—Serasa, Boa Vista, SPC—develop models calibrated to the average Brazilian population. That’s useful. But you don’t cater to the average. You cater to a niche, with a customer profile, average transaction value, and risk tolerance that are unique to you. When you apply a standard designed for the general market to your specific operation, the inevitable result is what we call “Stupid Strictness”: an overly conservative model that rejects good payers because it fails to see the nuances of your ecosystem.

This article is for risk officers, CFOs, credit managers, and heads of financial products who have realized that something isn’t quite right—that the approval rate could be higher without increasing risk, that the back office is overburdened, and that good customers are being turned down for reasons the sales team can’t explain. If any of these situations sound familiar to you, keep reading.

1. The root of the problem: how credit scores are calculated and why it matters to you

From Classical Statistics to Machine Learning: An Incomplete Evolution

The history of credit scoring models dates back to the 1980s, with statistical techniques such as logistic regression and linear discriminant analysis (LDA). These models were revolutionary for their time: for the first time, it was possible to convert historical behavioral data into a probability of default. The problem is that they operate on a strictly linear logic, and human financial behavior is rarely linear.

With the advancement of machine learning and artificial intelligence, financial institutions have begun using models capable of processing diverse data sources, identifying nonlinear correlations, and dynamically adjusting their forecasts. This is a real step forward. But there is one critical issue that this evolution has not resolved in traditional credit bureaus: the training dataset remains the same. It is still based on the market average.

The structural problem: the lowest common denominator

To operate on a national scale and serve tens of thousands of companies with completely different profiles, credit bureaus need stable models. And stability, in this context, comes at a cost: the model is calibrated to make as few errors as possible on average, which means it will make errors—sometimes significant ones—at the extremes. And your business niche is, by definition, an extreme.

A fintech company providing credit to small-scale farmers, a retailer with a well-established loyalty program, and a credit union specializing in loans for self-employed doctors—all of these operations have behavioral characteristics that a generic model simply was not trained to recognize. The result is what data scientists call a False Negative: the customer whom the credit bureau rejects, but who within their own ecosystem would be an excellent payer.

The commoditization of risk: when everyone uses the same yardstick

There is also a less obvious but equally devastating side effect: when your company uses the same credit bureau score as your competitor, you’re operating with the same margin of error as they are. There’s no differentiation in the risk model. There’s no competitive advantage. You’re making the same decisions as everyone else and, as a result, losing exactly the same good customers that everyone else is losing.

4kst calls this the commoditization of risk. It’s a silent trap, because most companies never stop to measure what they’re losing—they only see what they’re setting aside.

2. The hidden cost on the P&L: what the income statement doesn’t show but is eroding your margin

The most obvious cost of credit is delinquency. Every CFO keeps track of it. Every risk manager is familiar with it. But there is a set of costs that don’t appear in any standard report and which, when added up, can account for a significant portion of your EBITDA.

The bloated back office: paying people to fix algorithm errors

Models with low predictive accuracy create a structural reliance on manual analysis. When the automated scoring system rejects a customer whom the sales team “knows is a good fit”, the application goes to the reconsideration desk. The analyst reviews it. Sometimes they approve it, sometimes they don’t. And this cycle repeats itself hundreds or thousands of times a month.

The problem isn’t having a credit desk; it’s when the desk exists to systematically correct the errors of a model that should be its greatest ally. According to a QuerySurge white paper on operational pain points in banking institutions, finance teams lose up to 27% of their productive time dealing with problems caused by low-quality data and inaccurate models. This isn’t a credit cost; it’s an inefficiency cost disguised as a credit cost.

And the cycle feeds on itself: overworked analysts make more mistakes. Mistakes lead to more rework. More rework requires more analysts. You’re not scaling the operation; you’re scaling fixed costs to try to patch it up. According to the same study, the cost of replacing an experienced credit analyst can reach four times their annual salary, including recruitment, training, and lost productivity during the onboarding period.

The Lost Profits from False Negatives

How much does a “no” to a good payer? The answer isn’t zero. It’s that customer’s full LTV (Lifetime Value) multiplied by the number of times that happens per month.

Think about the acquisition cycle: your company invested in media, built a sales funnel, the lead arrived qualified, filled out the proposal, and the generic credit score rejected them. The CAC has already been spent. The revenue didn’t come in. And worse: that customer, who would have been a great payer in your portfolio, was likely approved by a competitor that uses a model with greater analytical granularity.

In a country where millions of people are in the process of becoming financially formalized—as self-employed workers, microentrepreneurs, or customers with limited credit history but a solid track record within their own ecosystem—the opportunity cost of false negatives is enormous. And invisible.

The Conflict Between Sales and Risk: A Cultural Cost

There is an internal friction that few people acknowledge, but which every company with a credit operation is familiar with: the tension between the sales team and the risk department. The sales rep brings in a customer. The credit score rejects the application. The sales rep thinks it’s unfair. They ask for reconsideration. The risk analyst reviews the case—sometimes using the same information, sometimes incorporating additional subjective factors—and makes a decision that may or may not align with the model’s recommendation.

This process leads to inconsistencies, friction between departments, delays in meeting SLAs, and, most seriously, a credit policy that, in practice, is not the one approved by management. It is the policy of whoever was on duty that day.

3. The Science of Assertiveness: What Is KS and Why Does It Determine the Limit of Your Growth?

In the world of credit, there is one metric that distinguishes amateur models from elite systems. It’s not the approval rate. It’s not the default rate. It’s the KS (Kolmogorov-Smirnov) test.

What is KS and how do you read it?

The KS measures the maximum distance between the distributions of good and bad payers in your model. In practical terms: the higher the KS, the more accurate the distinction between those who will pay and those who won’t. A model with a low KS acts like a coarse sieve that lets stones pass through along with the grains. A model with a high KS makes a surgical separation.

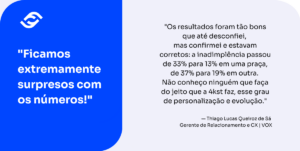

The direct impact on the business is immediate: with a high KS score, you approve applications with confidence. With a low KS score, you enter a cycle of “fear of approval,” management tightens credit, the approval rate falls below market potential, and delinquency rates still rise because the model fails to properly distinguish risks in the gray area.

Why do off-the-shelf scores end up with mediocre KS ratings?

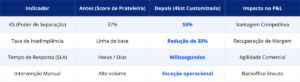

A typical credit bureau score, when applied in isolation to your business, tends to yield a credit score (KS) between 30% and 40%. This is reasonable for the market in general. But for your specific business, this figure represents an artificial ceiling. Not because the market won’t allow you to go beyond it, but because the model lacks the right data to do so.

The credit bureau’s scoring model is optimized for the bureau’s database—not yours. It doesn’t know that customers in a specific region of your niche consistently exhibit payment behavior that differs from the national average. It doesn’t know that customers with a recurring purchase profile in your CRM have a loyalty history that no credit bureau can see. It knows nothing about your ecosystem because it was never trained on it.

KS's leap forward with a customized credit model

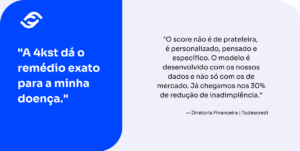

When we combine market data with your internal operational data and our more than 260 variables for individuals and businesses, KS consistently and measurably increases.

In real-world projects, we have observed an increase in the KS score from 37% to 55%—an 18-percentage-point gain that represents a substantial difference in the ability to make the right decisions. This increase is not merely theoretical: it is directly reflected in a reduction in PDD, an increase in approvals without a proportional rise in delinquency, and the release of capital that was previously set aside due to statistical uncertainty.

4. The Customized Credit Score: How It Works in Practice

A customized credit score does not replace the credit bureau; rather, it complements it by combining it with additional layers of intelligence.

Hybrid architecture: three worlds, one decision

The 4kst model works by combining three data sources into a single predictive engine:

- Customer data (internal): transaction history, payment behavior, average ticket size, purchase frequency, length of relationship, variables from your ERP/CRM. This is your gold, and credit bureaus don’t have access to it.

- Credit bureau data (external): market score, estimated income, restrictions, credit history in the financial system. The solid and necessary foundation of the analysis.

- 4kst proprietary data: more than 260 variables specifically calibrated to increase the KS value when combined with the above sources. These are not generic registry fields; they are statistically validated signals from dozens of real-world operations.

The model can operate in three configurations, depending on the maturity and objective of the operation:

- With Bureau + Internal Data + 4kst: Maximum accuracy. For operations aiming for peak performance.

- With Bureau + Internal Data: High accuracy at a reduced cost. For operations with an already optimized bureau volume.

- No Credit Bureau (Internal Data + 4KST): Search for savings in queries. For operations with a mature portfolio and rich internal data.

Security, the LGPD, and data governance

For the Chief Technology Officer and the Risk Manager, the natural question is: what happens to our data? The answer is straightforward. Data ingestion for the creation of the customized score takes place in a secure, encrypted environment that is fully compliant with the LGPD. Your operational data is used exclusively to build the intelligence of your own model and is never shared or contaminated with competitors’ data.

The integration is done via a secure, low-latency API that is compatible with cloud-native architectures (AWS, GCP, Azure) and any modern data stack—Snowflake, Databricks, Data Lake Houses.

5. Operational scalability: growing without increasing fixed costs

There is a key difference between credit operations that scale and those that merely grow: the former increases revenue without increasing fixed costs at the same rate; the latter hires more analysts for each new volume processed and makes no headway in terms of operating margin.

The customized credit score is the mechanism that makes this distinction possible. When the model is accurate enough to be trusted, human intervention ceases to be the rule and becomes the exception. And that is when the operation truly scales up.

What happens to the team when the model is reliable

One of the least discussed consequences of an overburdened back office is high turnover among technical staff. Senior credit analysts were not hired to manually review hundreds of applications a day. They were hired to think critically, fine-tune policies, identify patterns, and protect the portfolio in complex scenarios. When the model is generic and imprecise, these professionals become mere operators. And qualified operators quit.

With a highly reliable, customized model, the senior team can once again focus on what truly adds value: structuring complex operations, fine-tuning credit policy, and identifying opportunities for strategic adjustments. Analysts are no longer merely error-correctors for the algorithm; instead, they become the guardians of the risk strategy—a role that justifies their compensation and helps retain talent.

Speed as a direct competitive advantage

Decisions made in milliseconds keep the lead warm at the moment when purchase intent is highest. In the world of BNPL and PIX Parcelado, even a few seconds of friction cost conversions, and lost conversions at checkout are gone for good.

Highly reliable automation also eliminates subjectivity from the process: the credit policy approved by the board is executed with 100% accuracy, without variation based on the analyst on duty or the day’s volume. What was decided in the boardroom is exactly what happens in the operation—without deviations, without untraceable exceptions, and without the regulatory risk inherent in human inconsistency.

6. Impact on the bottom line: Measurable ROI, not just a promise

At some point in any conversation about credit technology, the inevitable question arises: how much of an impact does this really have on the bottom line? The honest answer is that it depends on where you start. But data from 4kst’s projects provides a solid benchmark.

What changes and how to measure it

- Reduction in delinquency: In projects where the company transitioned from a generic scoring model to a customized one, we observed reductions in delinquency ranging from 20% to 60%. Every percentage point decrease in delinquency has a direct impact on PDD, and PDD has a direct impact on net income available for reinvestment.

- Increase in qualified approvals: By capturing false negatives—good customers whom the generic score rejected—the company increases the approval rate without proportionally increasing risk. This is credit growth that is not accompanied by delinquency.

- Reduced operating costs: A lean back office, with less manual review, reduces fixed costs and frees up the team for higher-value activities.

- Increasing LTV: Approving the right customer on the first try is the start of a long-term relationship. The CAC has already been paid, and the LTV grows from there.

Success Story: Major Financial Institution

Anyone who has experienced it firsthand

7. The Brazilian market context: why 2026 no longer accepts off-the-shelf scores

Brazil has become a global hub for financial innovation. Digital credit fintechs have seen a 68% increase in lending volume, even amid high interest rates and tight liquidity. In this environment, off-the-shelf credit scoring is falling behind at a pace that most companies have yet to realize.

Open Finance Phase 4: The Shift to Real-Time Data

Phase 4 of Open Finance, which involves sharing data on investments, foreign exchange, and insurance, has created a financial snapshot of consumers that simply did not exist before. The problem is that traditional credit bureaus take months to incorporate these new data sources into their models, while customer behavior changes in a matter of days.

A customized credit score, integrated into the ecosystem via API, can ingest data and recalibrate the analysis in real time. It’s the difference between making decisions based on yesterday’s snapshot and making decisions based on today’s live feed. According to data presented at Febraban Tech 2025, the agility of data flows in Open Finance has already reduced the average time to approve credit by up to 30% in the country’s most advanced operations.

PIX Installments and BNPL: Credit That Takes Milliseconds

The Buy Now Pay Later market is projected to reach $4.66 billion in Brazil by 2025, and the BNPL 2.0 trend points toward retailers operating their own in-house credit solutions by using direct consumer behavior to feed their own scoring models. In this model, risk analysis must take place at checkout—invisible to the consumer—in less than a second.

Off-the-shelf scoring models were not designed for this workflow. They were designed for origination processes with margins of minutes or hours. A customized model natively integrated into the customer journey is what enables these new revenue streams—without friction, without cart abandonment, and without SLAs that are incompatible with the speed of digital consumption.

Alternative data: the blue ocean of the unbanked

About 40% of mobile lines in Brazil are prepaid and concentrated among classes D and E: people with limited or no credit history in traditional credit bureaus. For off-the-shelf scoring models, this audience is practically invisible. For a customized model that incorporates alternative data on telecommunications behavior, timeliness in paying utility bills, and utility consumption patterns, this same audience represents a segment of good payers that the competition is systematically ignoring.

Carriers such as Vivo, Claro, and Tim are already monetizing this data to create specific credit scores for the unbanked. Companies that know how to integrate these sources into their customized model will gain access to a market that credit bureaus simply don’t see.

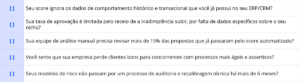

8. Diagnosis: 5 Signs That Your Business Is Being Drained by Off-the-Shelf Solutions

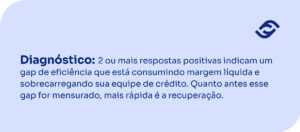

Before we talk about solutions, we need to be honest about the diagnosis. Answer the questions below, and if you check two or more, your business has a gap in assertiveness that is eroding your net margin:

Conclusion: The cost that wasn't listed on the bill now has a solution

We begin this article with a simple premise: there is a cost that doesn’t appear on the agency’s invoice. It will never appear because the agency doesn’t charge for it. Instead, the market bears this cost in the form of qualified leads that are rejected, overworked analysts, leads that don’t convert, and a higher-than-necessary default rate.

A customized credit score is not merely an incremental technological improvement. It is a strategic positioning decision: the difference between a company that accepts the market’s rules and one that sets its own.

Reducing delinquency by 30%, 40%, or 60%—depending on the starting point—is not a matter of luck. It is the result of training a model with the right data, on the right variables, for the right niche. At 4kst, we provide the science your company needs to to master its own risk. We are a DeepTech company born out of PUCPR’s AI research center, two-time champions of Febraban Tech (2022 and 2023), with proprietary Adaptive AI technology that ensures your model is not only more accurate today but continues to evolve tomorrow, without manual retraining and without degradation.

That cost that never showed up on the bill now has a name, a metric, and a solution. The question is when you decide to measure it.

About 4kst

4kst is a Brazilian DeepTech company born at PUCPR, a pioneer in the development of Adaptive AI. Through proprietary Data Stream Learning technology, we create predictive models that learn and update in real time. Unlike traditional Machine Learning, our solution eliminates performance degradation and reduces maintenance costs. Two-time winner of Febraban Tech and recognized by Finep, 4kst combines cutting-edge science and high performance to keep your company ahead in dynamic markets.

Related articles

Stay ahead

of the competition

Optimize your strategic decisions with the most assertive

forecasts on the market.

-

LGPD compliance

LGPD compliance -

BCB Resolution 85/2021

-

ISO/ISE 27001:2022 certification